Testamentary Trust Wills.

How can we help?

Most lawyers can prepare a Standard Will. However few lawyers prepare Testamentary Trust Wills and even fewer get it right.

Here at PB Ritz, we are specialist Estate Planning lawyers which means we specialise in drafting Wills. Over the past decade, we have prepared Testamentary Trust Wills for thousands of clients.

Our clients range from Mums and Dads with combined assets under $1 million, to ultra-high-net worth individuals with assets in excess of $100 million, and everything in between.

Whether you live in Sydney, Darwin, Perth, or anywhere else in Australia, we can prepare a Testamentary Trust Will for you. For more information on preparing a Testamentary Trust, get in touch with PB Ritz today.

Frequently Asked Questions

What is the difference between a Standard Will and a Testamentary Trust Will?

In simple terms, the difference between a Standard Will and a Testamentary Trust Will is that with a Standard Will, your children receive their inheritance in their own personal name following your death. In contrast, with a Testamentary Trust Will, your children have the option to receive their inheritance via a special trust that the Will creates following your death.

Testamentary Trust Wills have grown in popularity because it is favourable for your children to receive their inheritance via the special trust instead of in their own personal name.

Does having a Testamentary Trust Will complicate things for my children when I die?

No. Having a Testamentary Trust Will simply gives your children the option to receive their inheritance by a special trust following your death. Your children do not have this option if they receive their inheritance via a ‘Standard’ or ‘do-it-yourself’ Will.

We have created our Testamentary Trust Will with flexibility in mind. For example, your child can elect to receive part of their inheritance via the trust and part in their own personal name.

Your child may wish to do this if they have a debt they wish to repay, for example. Your child can also elect to bypass the trust all together and receive their inheritance in full in their own personal name, as they would under a Standard Will. However, this seldom takes place, as it is rarely in a child’s best interests to bypass a Testamentary Trust.

What benefits does a Testamentary Trust Will have to offer?

In summary our Testamentary Trust Will has 5 main benefits. For instance, you can use our Testamentary Trust Will to:

- Minimise the tax paid by your children

- Protect your children’s inheritance from loss by bankruptcy and potentially even divorce

- Choose who will care for your minor children should you and your partner die while you have a child under 18 years of age

- Choose the age your children will take control of their inheritance

- Choose who will manage your children’s inheritance

Why should I set up a Testamentary Trust Will?

There are many reasons why our clients opt to set up a Testamentary Trust Will over a Standard Will, however we have found there are typically 3 main reasons:

1. Prevent children from wasting their inheritance

Our Testamentary Trust Will can be used to protect children that are minors or reckless spenders. For example, you can elect the age that you would like your children to take control of their inheritance.

We recommend children are empowered to take control of their inheritance at 25 or 30 years of age as it is our belief that young adults typically lack the life experience and financial acumen to make sensible decisions when it comes to managing and investing their inheritance.

Using our Testamentary Trust Will you can appoint a trusted friend or family member to manage your children’s inheritance until they reach the desired age. Alternatively, you can appoint our Director, Phillip Briffa, to act in this capacity.

2. Prevent bankruptcy and divorce from eroding children’s inheritance

By leaving your estate to your children via our Testamentary Trust Will they receive asset protection benefits.

For example, your children’s inheritance is protected even if they become bankrupted after you die. This is not the case if your children receive their inheritance by a Standard Will.

Also, by leaving your estate to your children via our Testamentary Trust Will it is far more difficult for your children’s current and future spouses and de facto partners to get their hands on your children’s inheritance, should a relationship between a child of yours and their partner break down following your death.

3. Reduce children’s tax bill

The main reason why clients choose our Testamentary Trust Will is because it can be used as a tool to minimise tax. See below for more information.

How can a Testamentary Trust Will be used to minimise tax?

The main reason why our clients choose to have a Testamentary Trust Will prepared over a Standard Will is because it can be used as a tool to minimise tax.

The best way for us to illustrate how a Testamentary Trust Will can be used to minimise tax is by using some worked examples.

In the following two scenarios we demonstrate how strategies known as ‘Income Splitting’ and ‘Capital Splitting’ can be used to minimise tax.

Worked Example 1: Income Splitting

Samantha receives an income that places her in the top marginal tax bracket of 49% (includes 2% deficit repair levy). She has 3 children with her husband – aged 2, 4 and 6.

Samantha is about to inherit a $650,000 apartment from her recently deceased mother. The apartment is rented out for $45,000 per annum.

In the following scenarios, we illustrate how our Testamentary Trust Will could be used by Samantha to minimise tax by utilising a strategy known as ‘Income Splitting’.

Scenario 1: Samantha inherits via a Standard Will

If Samantha inherits the apartment via a Standard Will she will pay tax on the rent received each year pursuant to her personal income tax rate. The tax payable is calculated as follows:

Gross income $45,000

Tax on $45,000 $22,050 (@ 49% tax)

Net income $22,950

So, of the $45,000 gross annual income received by Samantha, $22,050 will be paid as tax meaning the net annual income will be $22,950.

Scenario 2: Samantha inherits via our Testamentary Trust Will

Let us compare the outcome where Samantha inherited the apartment (or any other asset for that matter) via a trust set up by our Testamentary Trust Will.

Under current taxation laws, Samantha may choose to allocate the trust’s income to her three minor children. For example, the taxable income for each child could be split as follows:

Gross income $45,000

Tax on $15,000 (Child 1) $ Nil (Within tax free threshold)

Tax on $15,000 (Child 2) $ Nil (Within tax free threshold)

Tax on $15,000 (Child 3) $ Nil (Within tax free threshold)

Net income $45,000

By ‘splitting’ the income received between her three minor children, Samantha can take advantage of her children’s tax-free thresholds. In summary, no tax is paid on the $45,000 rent received, meaning the after-tax cash saving for Samantha and her family is $22,050 and the net annual income of her family is $45,000 for the relevant financial year.

The right advice can make all the difference

It is worth noting that the above outcome could not be achieved if Samantha received her inheritance by a family trust set up by her mother during her lifetime. This is because distributions made to minors more than $416 in any given financial year from a family trust are taxed at the top marginal tax rate (penalty tax rate). Which is a reason why it is more tax effective for your beneficiaries to receive their inheritance by the special trust created by our Testamentary Trust instead of a family trust created inter vivos (i.e. during your lifetime).

Worked Example 2: Capital Splitting

Margaret, Emma and Lauren are sisters and they each receive an income that places them in the top marginal tax bracket of 49% (includes 2% deficit repair levy). They each have 3 minor children of their own and are married.

The sisters are about to inherit a $1,500,000 apartment from their recently deceased father. The apartment was purchased by their father 13 years prior for $600,000 as an investment.

The sisters wish to sell the property as they are each entitled to a 1/3rd share pursuant to the terms of their father’s Will. In the following scenarios, we illustrate how our Testamentary Trust Will could be used by the sisters to minimise their tax bill by utilising a strategy known as ‘Capital Splitting’.

Scenario 1: The sisters inherit via a Standard Will

If the sisters inherit the apartment via a Standard Will they will together pay tax on the capital gain of $900,000 pursuant to their personal income tax rates, less the 50% capital gains discount which applies, noting their father held the property for more than 12 months.

That means the total tax payable by the 3 sisters is calculated as follows:

Gross sale proceeds $1,500,000

Tax on $900,000 capital gain $ 220,500 (@ 49% tax, less 50% CGT discount)

Net sale proceeds $1,279,500

And the total tax payable by each sister is calculated as follows:

Gross sale proceeds $ 500,000

Tax on $300,000 capital gain $ 73,500 (@ 49% tax, less 50% CGT discount)

Net sale proceeds $ 426,500

So that means each sister will receive $426,500 after paying $73,500 in tax.

Scenario 2: The sisters inherit via our Testamentary Trust Will

Let us compare the outcome where the sisters each receive their share of the apartment via a trust set up by our Testamentary Trust Will.

Under current taxation laws, the sisters can allocate their share of the sale proceeds to each of their three minor children, to minimise their respective family’s tax bill. For example, the sale proceeds for Emma (or Margaret or Lauren) could be split as follows:

Gross income $ 500,000

Tax on $100,000 capital gain (Child 1) $ 12,316

Tax on $100,000 capital gain (Child 2) $ 12,316

Tax on $100,000 capital gain (Child 3) $ 12,316

Net income $ 463,052

By ‘splitting’ the capital proceeds received between their minor children, Margaret, Emma, and Lauren can take advantage of their children’s reduced tax rates to minimise tax. In summary, that means a tax saving of $36,552 for the families of each of Emma, Margaret, and Lauren (down from $73,500 in scenario 1 to $36,948 in scenario 2), which equates to an aggregate tax saving of $109,656 (down from $220,500 in scenario 1 to $110,844 in scenario 2), which represents a tax reduction of just under 50%.

The right advice can make all the difference

It is worth noting that the above outcome could not be achieved if Samantha received her inheritance by a Standard Will or a family trust set up by her mother during her lifetime.

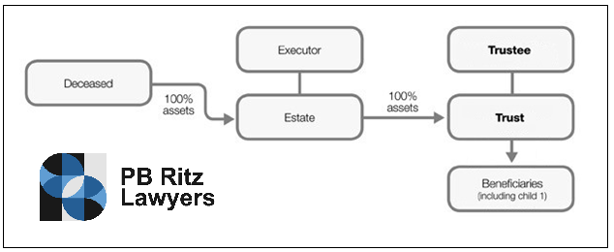

How does a Testamentary Trust Will work with 1 child?

The below diagram illustrates how our Testamentary Trust Will works in you have 1 child:

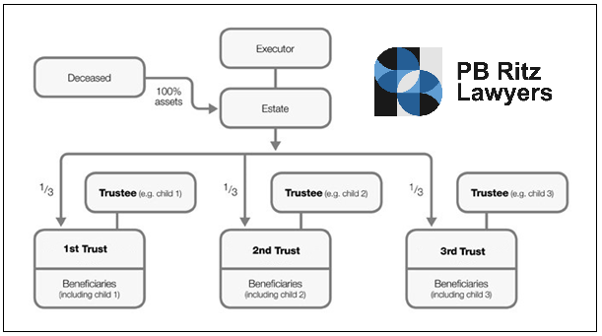

How does a Testamentary Trust Will work with 3 children?

The below diagram illustrates how our Testamentary Trust Will works in you have 3 children:

Are all Testamentary Trust Wills the same?

Not all Testamentary Trust Wills are the same. For example, we have designed our Testamentary Trust Will so that a separate trust is established for each of your children.

This is essential to ensure your children can make decisions independent of each other regarding how they will invest and spend their inheritance.

We recommend you avoid Testamentary Trust Wills that create a single trust for multiple children beneficiaries. These Wills often lead to disagreements and disputes between children beneficiaries which may lead to the Testamentary Trust being wound up (which means the tax benefits and asset protection benefits would be lost).

Is having a Testamentary Trust Will expensive?

No. Once our Testamentary Trust Will is prepared and signed, there are no additional costs.

When you die, your Testamentary Trust Will is read, and your beneficiaries are given the option to receive their inheritance by trust or in their own personal name (or by a combination of the two). If you die with a Simple Will, your beneficiaries are not given the option to receive their inheritance by trust, which means they lose the tax and asset protection benefits we spoke about above.

I own assets in more than one State, do I need a Will in each State?

No, this is not required. Our Testamentary Trust Will covers your assets Australia wide.

I own assets in Australia and overseas. Can my Australian Will cover my overseas assets?

It is important you make a Will in each jurisdiction where you own assets as succession laws differ from country to country therefore your Will needs to be carefully drafted in each jurisdiction where you own assets to ensure it complies with local succession laws.

For example, if you own assets in Australia and Singapore, you should have a Will prepared in Australia by an Australian lawyer to cover your Australian assets and a Will prepared in Singapore by a Singaporean lawyer to cover your assets in that jurisdiction.